Examples of liabilities include accounts payable, bank loans, and taxes. The accounting equation is also useful when considering how these assets will influence the company’s equity and overall financial strength when considering new investments. The ultimate goal is to ensure the investment adds value without disrupting the balance in the equation. This forward-looking application helps management align decisions with growth opportunities, which is necessary to sustain in the long run. An error in transaction analysis could result in incorrect financial statements. An accounting transaction is a business activity or event that causes a measurable change in the accounting equation.

What Happens if the Accounting Equation Is Not Balanced?

- On the other side of the equation, a liability (i.e., accounts payable) is created.

- Accounting books, annual accounts, compulsory chartered accountants…

- This is because accounting standards like IFRS and GAAP only recognize certain intangible assets if they have been acquired externally or can be quantified.

- Or in other words, it includes all things of value that are used to perform activities such as production and sales.

- As a core concept in modern accounting, this provides the basis for keeping a company’s books balanced across a given accounting cycle.

- This business transaction increases company cash and increases equity by the same amount.

From setting up your organization to inviting your colleagues and accountant, you can achieve all this with Deskera Books. You can witness the easy implementation of the tool and try it out to get a renewed experience while handling your accounting system. Debits are cash flowing into the business, while credits are cash flowing out. The merchandise would decrease by $5,500 and owner’s equity would also decrease by the same amount. On 22 January, Sam Enterprises pays $9,500 cash to creditors and receives a cash discount of $500.

Purchase of Equipment in Cash

This is particularly important for businesses making investment decisions or evaluating projects with cash flows spread over multiple years. Therefore, while the accounting equation is a fundamental tool, a lack of consideration for the time value of money limits its usefulness in long-term financial planning. The future cash flows related to assets are debts that may be recorded at their current value, but their true worth can change over time due to inflation or investment opportunities.

Let us take a look at transaction #1:

The capital would ultimately belong to you as the business owner. In the case of a limited liability company, capital would be referred to as ‘Equity’. Shareholders’ equity is the total value of the company expressed in dollars. Put another way, it is the amount that would remain if the company liquidated all of its assets and paid off all of its debts.

The accounting equation And how it stays in balance

Debt is a liability, whether it is a long-term loan or a bill that is due to be paid. The major and often largest value assets of most companies are that company’s machinery, buildings, and property. Accounts receivable list the amounts of money owed to the company by its customers for the sale of its products. Assets include cash and cash equivalents or liquid assets, which may include Treasury bills and certificates of deposit (CDs). However, this scenario is extremely rare because every transaction always has a corresponding entry on each side of the equation. This formula represents the accounting identity, which must always be true for all entities regardless of their business activity.

4: The Basic Accounting Equation

Without adjusting for these factors, financial statements may give an incomplete picture of a company’s financial health. This can give a false view of the company’s current financial health. As market conditions keep fluctuating, asset value also changes, but these changes are not reflected in the financial statements when historical cost is used. This disconnect can also result in investors or stakeholders having an inaccurate understanding of the company’s true market value.

However, they are not always captured in financial statements. This is because accounting standards like IFRS and GAAP only recognize certain intangible assets if they have been acquired externally or can be quantified. For example, if you subtract liabilities from assets, you will get equity, and vice versa. Understanding how to use this formula 6 ways to write off your car expenses and other necessary basic accounting terms is crucial for finance professionals as it helps to verify the accuracy of records. To prepare the balance sheet and other financial statements, you have to first choose an accounting system. The three main systems used in business are manual, cloud-based accounting software, and ERP software.

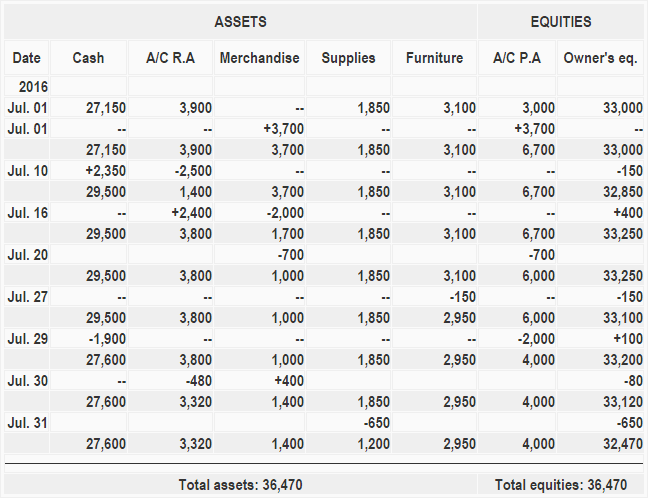

If a company’s stock is publicly traded, earnings per share must appear on the face of the income statement. In above example, we have observed the impact of twelve different transactions on accounting equation. Notice that each transaction changes the dollar value of at least one of the basic elements of equation (i.e., assets, liabilities and owner’s equity) but the equation as a whole does not lose its balance. The dual aspect of accounting is very important since it ensures that all of the transactions are tracked properly and portrayed.

A company’s quarterly and annual reports are basically derived directly from the accounting equations used in bookkeeping practices. These equations, entered in a business’s general ledger, will provide the material that eventually makes up the foundation of a business’s financial statements. This includes expense reports, cash flow and salary and company investments. For a company keeping accurate accounts, every business transaction will be represented in at least two of its accounts. For instance, if a business takes a loan from a bank, the borrowed money will be reflected in its balance sheet as both an increase in the company’s assets and an increase in its loan liability. This straightforward relationship between assets, liabilities, and equity is considered to be the foundation of the double-entry accounting system.

For every business, the sum of the rights to the properties is equal to the sum of properties owned. For the past 52 years, Harold Averkamp (CPA, MBA) hasworked as an accounting supervisor, manager, consultant, university instructor, and innovator in teaching accounting online. He is the sole author of all the materials on AccountingCoach.com. Parts 2 – 6 illustrate transactions involving a sole proprietorship.Parts 7 – 10 illustrate almost identical transactions as they would take place in a corporation.Click here to skip to Part 7.

Because you are taking $100 out of business, your owner’s equity will decrease by $100. Equity refers to the owner’s interest in the business or their claims on assets after all liabilities are subtracted. The accounting equation matters because keeping track of each transaction’s corresponding entry on each side is essential for keeping records accurate.